Back in the Grinder

By Crest Capital Advisors on June 10, 2022

Dow: (4.58%) to 31,392.79

S&P 500: (5.05%) to 3,900.86

Nasdaq: (5.60%) to 11,340.02

Russell 2000: (4.40%) to 1,800.28

10 Year Yield: 3.16%

Outperformers: None

Underperformers: Financials (6.77%), Technology (6.38%), REITs (6.10%), Consumer Discretionary (6.07%)

US equities were sharply lower this week, with a hotter-than-expected May CPI report knocking the legs out from under the recent rally and raising fears of a more-hawkish Fed and a possible recession ahead. The S&P is now down for 9 of the past 10 weeks, logging its worst weekly performance since January and seeing an evaporation of much of its rally off the May 20th low. Treasuries were weaker with the 10-year Treasury again north of 3%, closing Friday at 3.16%. Oil was higher as well, with WTI settling up 1.4% amid ongoing fears of further European disruption, strong Asian demand, and lagging OPEC+ production. All S&P 500 sectors were lower offering investors few places to hide.

Overall, it was an extremely uneventful week, at least until the end. Directional drivers were largely absent with trading fairly listless through midweek as investors waited for May’s CPI report to be released on Friday. The week saw a somewhat better regulatory tone out of China (though also lingering zero-Covid concerns on some new Shanghai restrictions) and discussions around economic normalization. But then Friday morning brought the May CPI report to trump all of that: a hotter-than-expected reading both on the headline and core measures (more on this below), sparking renewed concerns about a Fed having more hiking ahead of it, and consumers increasingly bending under the weight of higher prices. There will now be much more attention on next week’s FOMC meeting, which some analysts today have even suggested may be compelled to make a 75bp hike (vs expectations for 50bp) as it strains to get a handle on prices.

A major element of the bull thesis has been the thought we are past peak inflation and peak Fed, though this theory has taken hits beyond this week’s CPI report. There have been some signs of price softening in certain spots (Bloomberg this week pointed to easing prices for chips, shipping containers, and fertilizer), while retail inventory overhangs may suggest a more promotional environment ahead and announcements of slower hiring/layoffs could be a sign of an easing labor market. But at the same time, oil prices have been unrelenting and there are signs that lower-income consumers may already be downshifting their discretionary spending as gasoline gains more wallet share. And note that this week’s other major economic release, consumer sentiment, hit a record low amid a four-decade high in respondents concerned about inflation.

Inflation, Inflation, Inflation

What’s the latest?

The US Consumer Price Index (CPI) rose +1.0% month-over-month and 8.6% year-over-year (a new high) in May. The core CPI (more focus here from the Fed’s perspective) also surged +0.6% month-over-month, and 6.0% year-over-year (down a tick from last month’s 6.2% rate). Market participants were looking hoping for a smaller increase and a downside surprise. Instead, we got the opposite.

As noted above, core inflation, more than the headline, will help inform future Fed decisions. But both surprised to the upside this month. Bottom line: U.S. core inflation is still too high, and monetary policy will need to continue to tighten as a result. The Fed has set up +50 bp rate hikes for the next several meetings, and that looks appropriate (if not slow) given today’s data.

Why do we have high inflation?

We have the inflation we have today because we made the decision to create a scarcity of goods and services by locking down the global economy, and then we helicopter dropped trillions of dollars to businesses and households so they could go on spending money anyway! We made a conscious decision to have inflation! But, the alternative was to stay in an outright depression. Had we done that, we wouldn’t have had inflation but we would venture to guess that the economy and asset markets would look a whole lot worse today had we chosen that path. But now that we didn’t have the depression, all everyone wants to talk about is inflation.

It remains to be seen if the supply-driven inflation can be rectified structurally before lasting damage occurs. Unemployment is, for example, still at historically low levels, so for the time being, many consumers are still in fairly good economic health. Unemployment is hovering near record-lows and while recently impaired, the consumer and corporate balance sheets (collectively) are in great shape today.

When your only tool is a hammer, every problem looks like a nail!

The Federal Reserve, which has never forgotten lessons learned in the late 1970s and early 1980s, has never abandoned inflation as one of its targeted objectives. Some would argue that they waited a quarter or two too long, hoping inflation would be more transitory, but when they did act, they were ready with an aggressive game plan to raise interest rates. While the Fed has a long memory, most market participants today have never operated in an environment of rising rates and inflation, as that last occurred in the US during the Carter and Reagan administrations.

Every crisis is different and looking to the past to see what to expect in the current situation is always going to be an inexact comparison. Most of us invest for the long haul—and if we have matched our investments with the horizon of our liabilities (e.g. retirement funding, education funding, etc), then we should have a temperament that allows us to stick to our strategic objectives and not be tempted to reverse course during times of market stress.

Where we go from here…a theory….

The year-over-year rise in money supply is highly correlated to a rise in inflation, though typically with a 13-month lag. IF we look at where this model of M2 money supply would project inflation today (based on M2 data 13 months ago), we would expect core inflation of ~ 5.2%. Today it is actually 6%, so not too far off. If we continue to extrapolate this data forward, based on M2 growth today, the equation tells us where inflation is headed in 13 months from now. And that figure is 2.5%!

Since 2017, federal debt growth and M2 money growth have been highly correlated, and in turn M2 growth has been even more highly correlated with core inflation, with the aforementioned 13-month lag. With no new major spending initiatives in over a year, debt and M2 growth are decelerating rapidly. The regression equation calculates that in 13 months core CPI will be 2.5%, slightly below the Fed’s target when stated in CPI terms.

Headline CPI will keep seeing support from energy in the near term. The big inflation headwind will come from goods deflation, as retailers finally admit to involuntary inventory builds, and the need to discount. (See Walmart and Target’s latest earnings reports for confirmation of this!) Net, we still see headline inflation falling by year-end and into next year. The Fed’s rate hikes between now and then are still well within the acceptable range for where the economy stands today.

Is There Opportunity Here?

Inflation and rising interest rates can be destructive to investment returns, but we are tactically eyeing real estate, real assets, and private debt for potential areas of relief.

Tactical Outlook

The risk of a US recession has risen but that does not mean one is imminent. Even after recent falls in stock and bond prices, household and corporate balance sheets are still fairly robust. And, as anyone who has recently tried to book flights, cars, or hotels in the US can attest, services demand remains strong. Order backlogs are not growing at the pace they were six months ago in both the manufacturing and service sectors, but they are still expanding. And capacity remains tight in many areas.

We continue to see the US economy on a narrow path to a soft landing. The 390k increase in nonfarm payrolls in May beat expectations, and the unemployment rate has now been flat at 3.6% for three months in a row. The underemployment rate U6 edged up again, and average hourly earnings registered another benign 0.3% gain. Moreover, job openings have started to decline. The official JOLTS series dropped sharply in April and timelier private-sector measures suggest that this drop continued in May. More anecdotally, many technology firms seem to be cutting back on new hiring and job openings. But all of this is healthy to bring labor supply and demand back into balance.

The price news also looks more encouraging. Most notably, statistical measures of sequential PCE inflation—especially the trimmed core index—have eased over the past few months. Broad supply chain measures have improved, with the supplier delivery components of the monthly business surveys declining from high levels. However, one area where the news has been more mixed is the auto sector, as semiconductor supply is improving, but shortages of auto parts from Ukraine and China are putting upward pressure on prices. This is one reason why we are not terribly surprised by the upside increase in the May CPI data.

We fielded a number of questions about an imminent recession following the Q1 earnings reports from Walmart and Target. But the macroeconomic significance of these disappointments is limited, in our view. Part of the problem was a large increase in shipping costs, consistent with what we see in the economic data but not really new information. Then there was the spending shift away from discretionary items in April noted in the Target earnings call. Since that call, however, we have learned that real personal consumption in April was actually quite solid; in any case, we should expect goods consumption to underperform service consumption as the economy emerges more fully from the pandemic.

Open Mouth Operations

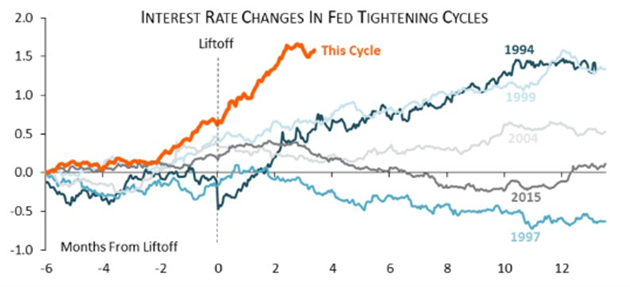

We all know that interest rates have risen fast this year, following the Fed hawkish pivot in the fall of 2021. But just how fast? To put some context into that question, we constructed an index of various interest rates that affect the US economy the most. In particular, we included government interest rates, corporate interest rates (commercial paper and bonds of various credit quality), and consumer interest rates (mortgages, auto, and personal loans). The conclusion is in the chart below: We are going through the fastest tightening cycle since 1994.

Of course, the Fed has actually done relatively little so far—only 75 bps of actual tightening. But markets have responded sharply to the Fed’s hawkish guidance and have quickly internalized all the future tightening that the Fed is expected to do in the quarters ahead. In other words, what we are going through shows the power of forward guidance: Central banks can tighten as much as they want just with words; as soon as they have credibility, the market will quickly reflect that guidance into asset prices, and the economy will respond accordingly.

There were periods, especially in the late 1970s and early 1980s, when Fed policy adjusted faster than now and may have had a bigger impact on overall interest rates, but at least we can say that we are going through something unprecedented in the past 32 years, which spans the careers of most of us.

From a practical economic perspective, what does this mean? Interest rates are an important part of financial conditions, and their increase has contributed significantly to the recent tightening in those conditions. The chart below shows the index of US financial conditions, which, in addition to the interest rates mentioned above, also includes equity prices, the value of the US dollar, and other short-term market rates and spreads. Clearly, financial conditions have tightened significantly since late last year but don’t overlook the fact they remain well below prior recessionary periods.

Don’t Overlook Small-Cap

If you’re like us, and you don’t think a deep recession is on the horizon, then it is highly unlikely that small-cap stock valuations will remain at these lows. A quick glance at the chart below and you will see that valuations for small-cap stocks collectively are at levels commensurate with the Great Financial Crisis of 2008-9, and effectively at 25-year lows! There is a big opportunity in or around the levels we’re seeing today.

First In, First Out?

The prevalent view for a decade was that China was set to take over the world, guided by infallible policymakers. Today, many investors are taking the opposite view. Between China’s tech crackdown, President Xi Jinping’s focus on “common prosperity”, interminable Covid lockdowns, and heightened tensions over Taiwan, the general perception has shifted to a widespread belief that China is now “un-investable.”

Interestingly, however, Chinese equities have managed to claw back some losses over the past two months despite these negative headlines, while the Chinese government bond market has remained a bright spot in an otherwise grim global landscape (see charts below). If China is about to invade Taiwan, it seems that the Chinese Government Bond (CGB) market did not get the memo. Rather than be un-investible, could China, in fact, lead the way out of today’s bearish global environment? And if so, what could serve as a catalyst for such a rally? Don’t look now, but China tech stocks are broadly outperforming US peers and many were up on the day for Friday, while US stocks were dropping significantly.

The first chart below is of the China 10-year government bond. We’re starting to see a breakout on the back of economic optimism after 18 months of downward pressure.

The next chart shows the China Tech ETF relative to the Nasdaq 100 ETF. China tech stocks are showing solid relative strength compared to US peers. This has all the looks of a rounded bottom and the beginning of an outperformance cycle to us.

2%

As of today, we are on pace for a second consecutive quarter of negative returns for stocks & bonds. Of the 185 quarters since 1976, a negative quarterly return for both stocks and bonds has occurred just 19 times, including the first quarter of 2022. Furthermore, over the same period, there are just four instances (2% of observations!) where both stocks and bonds are negative for two consecutive quarters, with three of those four instances associated with a recession. If this quarter closed today, it would be the fourth where both stocks and bonds saw negative returns.

Crazy Stats of the Week

Here are this week’s crazy stats:

- The new lowest reading in the history of the University of Michigan Consumer Sentiment Index was posted today with a dismal 50.2 v. 58.5 estimated by economists.

- Sky-high airfares are the latest headache for globetrotters, with direct flights between New York and London in late June costing more than $2,000 in “economy.” At that rate, it is no longer economic to ride in the “economy.”

Quote of the Week

“There’s no such thing as a free lunch.”

– Milton Friedman

Calendar of Events to Watch for the Week of June 13th

On the Corporate calendar, earnings slow to a trickle while Brokerage Conferences and Analyst/Shareholder Events move to the forefront on the corporate calendar with busy weeks ahead in both. Investors are looking for any clues into real-time business conditions (earnings are backward looking) to gauge the overall health of the economy right now. On the US Economic Calendar next week, Wednesday’s FOMC Meeting will be front and center with additional data readouts on the Producer Price Index (PPI) taking on added importance in light of this week’s hotter than hoped for Consumer Price Index (CPI) report.

Monday 6/13 – No major economic reports today.

Tuesday 6/14 – The Producer Price Index (PPI) is expected to come in hot at 10.8% headline and 0.6% month-over-month, with the Core (Ex-food & energy) expected at 8.7% year-over-year.

Wednesday 6/15 – US Retail Sales data for May is expected to show a 0.7% monthly increase. But the highlight of the day will be the conclusion of the FOMC meeting and the subsequent press conference with Jerome Powell. After this week’s CPI report, market expectations are ratcheting back up for more aggressive action at future Fed meetings.

Thursday 6/16 – Housing Starts data for May will be out with expectations for a 0.35% month-over-month increase. The weekly jobless claims data is starting to receive more attention as well as markets focus on employment and the overall health of the US economy.

Friday 6/17 – Industrial Production for May is expected to post a 0.5% monthly increase, down from 1.1% last month. US Leading Indicators are expected once again to contract by -0.35%, roughly in-line with last month’s -0.3% contraction.